There is a tendency to believe retail financial planning advice must be feature-rich to be meaningful and achieve scale. In reality, the banks that are leaders on retail advice become successful before they finish rolling out all the features shown in the figure below. Instead, they take a sequential and organized approach to rolling out their offer.

Most tier 1 banks already have a good range of table stakes features, like financial literacy articles, product selection tools, and expense management apps. However, leading banks that offer personal financial planning advice are more likely to prioritize the delivery of enabling features over the creation of innovative features.

By enabling features, customers can browse and access a bank’s self-serve advice tools. These also serve as channels that customers will use to seek advice from a person, although this will most often still be an online experience. This is key to driving adoption for other features and giving the client a sense that they are receiving holistic advice. Examples of enabling features are advice centers or advice portals that allow access to articles, advice tools, and even real-time goal monitoring. Financial checkups or financial journeys are enabling tools that will enable banks to understand the client’s advice needs. Finally, collaboration tools and processes allow advisors to have meetings remotely, digitally, and effectively with clients.

Once banks have matured their table stakes and enabling features, the next step is to expand into a more innovative territory. These features involve more complex types of advice like financial or retirement planning, or ‘people like you’ − an offering that helps clients make financial decisions and reach goals based on the data gathered from a comparable peer group.

Segmentation by behavior

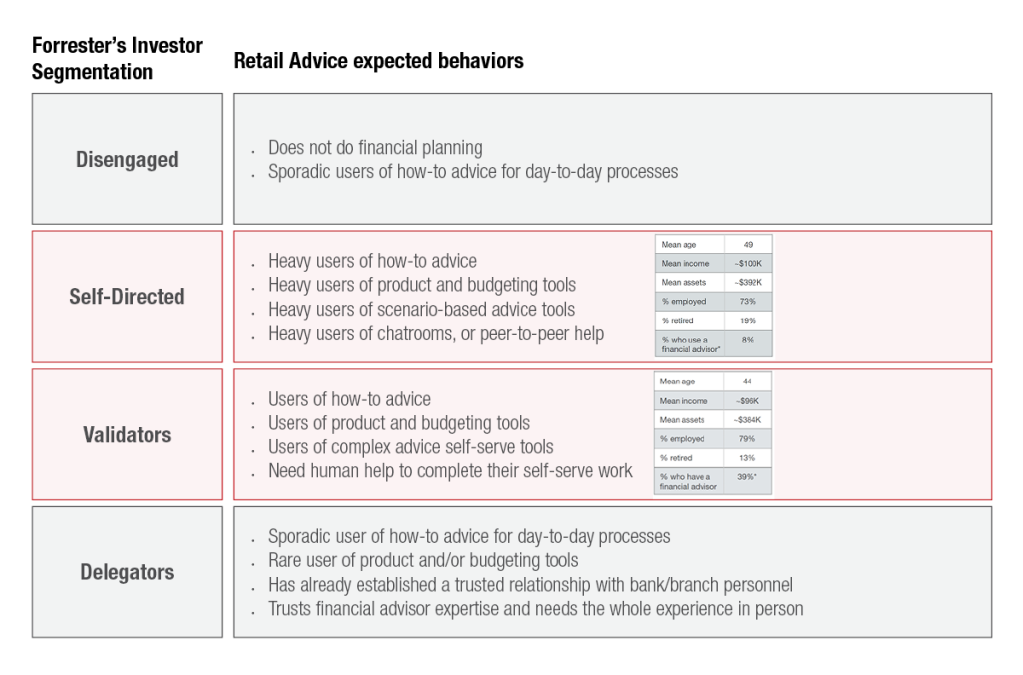

Banks with successful retail advice strategies achieve great adoption rates when segmenting the market by behavior. Historically, they segmented clients by wealth-factor, providing financial planning advice predominantly to the retail market’s wealthiest 20 percent. However, that resulted in a branch-centric model. Today, customers are moving away from the branch-centric model towards more accessible services via the internet or phone. Segmentation by behavior has helped banks focus on those clients willing to receive financial advice using a hybrid model of self-serve and assisted advisory.

A good example of segmentation by behavior is Forrester’s Investor’s Segmentation (included in Table 1 above). While this was originally created to segment investors, it’s still a great tool to use to segment customers for the retail advice space. Banks with successful retail advice strategies focus primarily on the self- directed segment (those that will advise themselves entirely) and the validators (those that are willing to do a piece of the advice by themselves but will eventually require guidance). These customers are most likely to adopt the hybrid financial planning advice model that banks are able to offer.

Journeys are not linear

Initially, banks thought they would manage and control the way retail clients consumed advice but soon realized that the needs, behaviors, and financial literacy across clients are highly diverse. A retail client’s journey is not a linear one; it is complex and unpredictable. Some retail clients will go directly into financial and retirement planning without researching beforehand. Other clients will take a more methodical approach, electing to do their research first and then contacting a virtual advisor to consult on the next steps.

The main takeaway from leader banks is to be prepared for all types of client journeys. One way to achieve this is through an advice center that resembles a restaurant menu − presenting a selection of recommended offerings. Clients can select what suits them best or even tailor a solution from scratch.

Technical building blocks

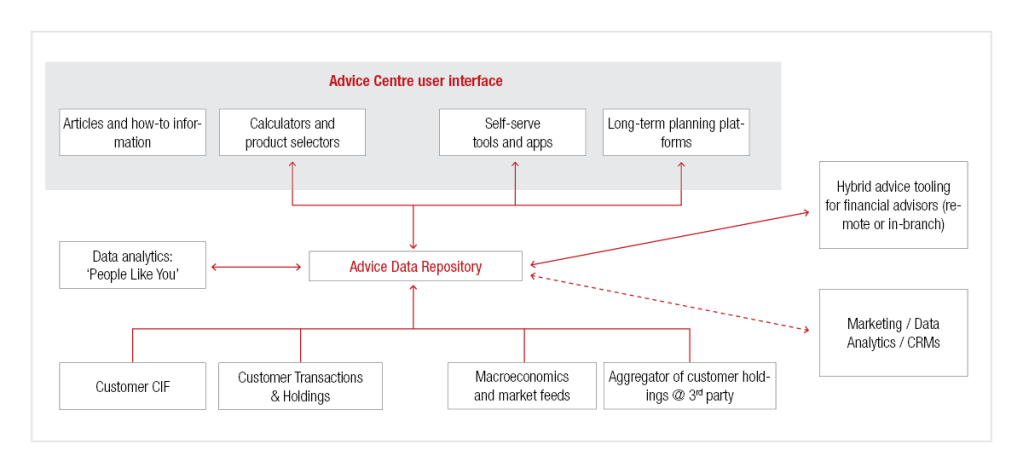

Retail advice does not require complex architecture. You can unlock most of the retail advice value through a cohesive front-end, robust data integration, emphasizing extracting relevant data from different advice apps or features into a centralized repository. This information will help improve the financial planning advice tools currently available and provide information for future long-term planning platforms. It also reduces the need to capture data from customers repeatedly, facilitates innovative features like ‘people like you,’ unlocks actionable customer volunteered data for CRM and marketing and helps unlock the potential functionality of long-term advice platforms.

This column was written by Nicolas Beltran and Adam King. Beltran is a managing principal and King is an associate at Capco, a global technology and management consultancy specializing in driving digital transformation in the financial services industry.

To contact the authors this story:

Nicolas Beltran can be reached at nicolas.beltran@capco.com

Adam King can be reached at adam.king@capco.com

This column does not necessarily reflect the opinion of FinLedger’s editorial department and its owners. To contact the editor responsible for this story: editor@finledger.com