The global open banking market is projected to reach $43.15 billion by 2026, according to a recent report from Allied Market Research. That’s up six-fold compared to $7.3 billion in 2018.

What has led to the global open banking market’s burgeoning growth?

There are various major factors. For one, people are increasingly adopting more apps and services. Also, favorable government regulations, improved customer engagement with open banking APIs and more collaborations between banks and fintech companies all have the potential to create new opportunities going forward.

Open banking allows data to be digitally transferred related to the bank account of a customer and gives third parties like banks and fintechs access to account information. Check out our open banking explainer here.

The COVID-19 pandemic has boosted growth in global open banking, for a variety of reasons, including the increased demand for contactless payments and payments through chip and pin machines.

There’s a handful of fintech companies that have created digital solutions via open banking and asked for support from the government, which will help market growth as well. Also, the planned number of open banking solutions still due to launch is also expected to increase market presence.

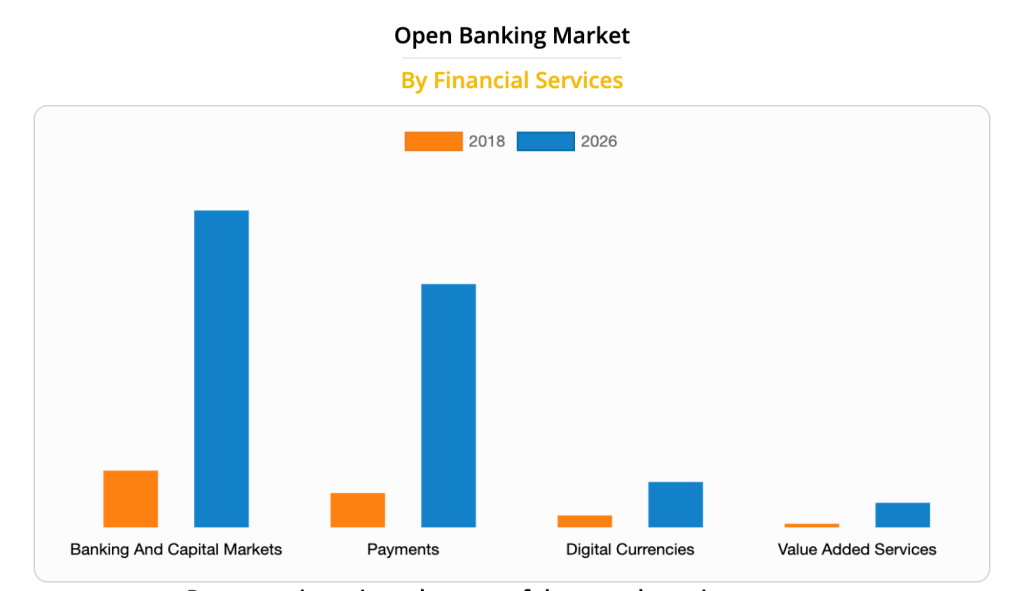

Accounting for over half of the global market, the banking and capital markets segment dominated the market in 2018. But notably, the payments segment is expected to demonstrate the highest compounded annual growth rate of 27.3 percent between 2019 and 2026, according to the report.

Regionally speaking, Europe held a large share of the global open banking market in 2018 due to government directives that made banks mandatorily open APIs.

With an expected CAGR (compounded annual growth rate) of 26.5 percent, North America is expected to register the highest growth during the forecast period – between 2019 and 2026 – mainly because of its adoption of technologies, among other factors.

By distribution channel, the distributors segment is expected to see the highest CAGR of 27% during the forecast period, mainly due to the surge in awareness related to the adoption of the role of a distributor among banks and increased efforts taken by banks to extend their digital market presence by distributing third party services.

That’s a change from 2018, when the app market held the largest share, making up more than two-fifths of the global open banking market, due to a climb in the adoption of smartphones across the globe and an increase in awareness regarding use of banking apps.

The report listed these companies at the largest major market players:

- BBVA Open Platform

- DemystData

- Credit Agricole

- Finastra

- Figo GmbH

- Jack Henry & Associates, Inc.

- FormFree

- MineralTree

- Mambu GmbH

- NCR Corporation